Analysis:: Colorado Springs economic growth slows, labor market still tight

This is the last economic dashboard for 2023 with a peek at what’s to come for 2024. In December, regional economic growth rates are released by the Bureau of Economic Analysis for the prior year as this data lags quite a bit. This measure of gross metropolitan product, or GMP, is a key indicator of how much a region grew relative to the year prior.

In 2021, most of the nation far outpaced trend growth with U.S. GDP at 6.2%, Colorado at 5.8% and Colorado Springs MSA at 5.1%. These stellar growth rates were largely a result of lingering pandemic stimulus and strong employment mostly due to demographics. In 2022, however, I was somewhat shocked to see that our region’s growth rate was at 1.0% while the U.S. (2.1%) and Colorado (2.2%) returned to trend growth. Other regional indicators showed strength in the local economy, so at first glance this didn’t make much sense to me.

But as I thought about it some more, some explanations emerged. In a nutshell, all the U.S. had a shortage of (particularly) qualified workers, and small business surveys have consistently supported this. Many businesses say they could have grown more if they had the labor they needed. Our state and region have had an especially tight labor market. Using job opening information from labor market analyst Lightcast and unemployment numbers from the Bureau of Labor Statistics, on average the U.S. had 0.71 workers for each open position in 2022 whereas Colorado had 0.41 and Colorado Springs had 0.42 workers for each open position.

The decline in working-age people in Colorado is cited as one of the largest risks to our long-term economic growth, according to the latest report from the state economists. I further address this below. This year, the labor market across all regions has normalized somewhat and our region is currently at 0.66 workers per job opening. This may help us out some as we enter 2024, but remember that tw-thirds of one person per open job does not make a happy business owner — and that’s if that worker is qualified for a given position. Another indicator of a cooling (but still tight) labor market is the fall in job openings across the U.S., which stood at 8.7 million. The “fall” is relative to the highly abnormal level of 12 million in March 2022, but still elevated compared to the pre-pandemic average of 5 million openings (since 2006).

There is another contributor to our 2022 lackluster growth rate also tied to the labor market. Due to the structural changes in most developed nation’s demographics with fewer working-age people relative to retirees, and the labor market volatility of the pandemic, there was likely more labor hoarding in 2022. Businesses had such a tough time finding qualified labor (or any labor for that matter) that they were reticent to let go of any workers or reduce hours in fear that it would be tough to find new talent — even if revenue growth was slowing. At the same time, many employers had to pay higher wages that precisely stem from labor shortages. This, too, would restrict business revenues and overall growth.

Our subpar regional growth was also largely attributable to lower in-migration. Our region typically has 10,000 to 11,000 new residents move into El Paso County each year, but in 2022 we had 3,400 new residents. This, of course, exacerbated the labor shortage and reduced the level of consumption that typically goes with new residents. Tied to this is the slowdown in construction precipitated by higher interest rates with crimped consumption on the demand side (fewer new residents, and fewer existing residents buying homes), and crimped production on the supply side (less construction-related expenditures). Interestingly, the construction industry was bumped off the list of top growing industries and replaced by accommodation and food (with 11% growth from 2017 Q2 to 2023 Q2).

Lastly, it’s possible that both public and private hiring was boosted by pandemic-related government programs that helped the strong regional employment gains of 10,480 new jobs in 2022 — a level almost double what is needed to match population growth (5,600). In 2022, finance and insurance, construction, wholesale, and retail trade were industries that saw outright declines in GMP output. Lower rates of growth (compared to 2021) were seen in professional and business services, education, health care and social assistance, and hospitality.

The issues of demographics and higher cost of living are hitting us even faster than I thought. Our state has outperformed the nation in terms of economic growth rates and employment, so we are fortunate to have a baseline of businesses across many sectors. This is certainly a comparative advantage, but it will require a pipeline of workers for decades to come. And since “prime working-age individuals” are typically 25-54, housing affordability is intrinsically tied to future in-migration, labor availability and overall economic vitality.

Which brings me to opportunities in our region. Specifically, the in-migration advantage we are currently projected to have relative to 59 other counties in our state. Between now and 2030, El Paso County is one of the five counties projected to have robust net migration with between 30,000 and 52,411 new residents. Indeed, our paltry population growth in 2022 is supposed to resume to roughly 10,000 new residents in 2025, according to the State Demography Office. I buy this with the caveat that other counties across the nation have had to sharply reduce population growth estimates due to higher costs of living. That’s the downside. The upside is that if we indeed can increase our affordable housing stock, we are positioned as one of the high-growth regions in Colorado and indeed across the U.S. Let’s meet that challenge, I say.

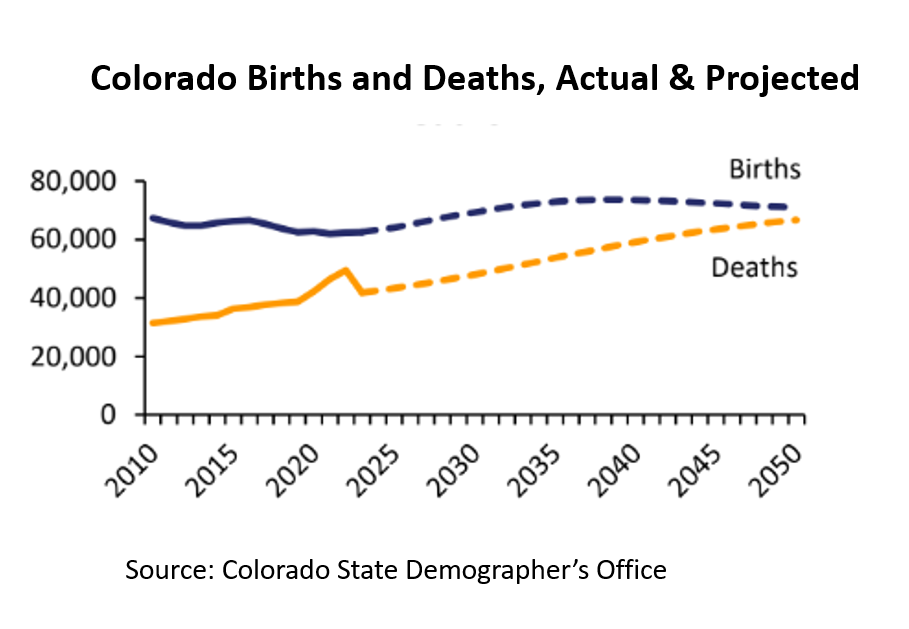

And as the visual shows, attracting and keeping especially child-bearing age adults will be key within our state as it has been in the past. Within Colorado, stagnant birthrates relative to deaths are a challenge. Younger adults between 20 and 39 accounted for the largest share of net in-migrants (60%) from 2000 to 2020. Past decades of younger residents moving to our state are now coming to roost with a sudden aging of the population as those 1980s and 90s transient go-getters become retirees. Over the next five years alone, there will be 40,000 annual retirements in Colorado. We currently have 1 million residents age 65+ (16.4% of the CO population) and will have 1.6 million (21.1%) by 2050. As the state economic report says, “the 65+ cohort will simultaneously put downward pressure on government revenue growth as older adults typically pay lower income taxes due to retirement or fixed incomes, generate lower sales tax collections through reduced spending, and qualify for more tax benefits such as property tax exemptions like the Senior Homestead Exemption.”

I will add, however, that older Americans have stepped up in terms of working past normal retirement ages as have working-age women. So, although the overall U.S. labor participation rate is anemic compared to other developed nations, older workers and women have increased their participation in the past few years, and that has helped. The headwind is more about the tsunami of retirees relative to previous decades.

I believe another antidote to these structural changes includes real-time response to changes in the labor market. This includes assiduous attention to the high-demand skills as reflected by job postings with active local implementation of new training/certification programs such that business growth can be at its full potential.

And if I zoom back out and look to 2024 and 2025, I have to say that next year, in particular, will look flat compared to the elevated consumption and growth levels the U.S. has experienced post-pandemic. I see various factors that ensure some level of volatility in inflation including business owner surveys that show elevated prices paid (which get passed onto consumers), geopolitical threats in gas-producing regions, a structural housing shortage, and deglobalization. In turn, this ensures that interest rates will not return to zero or near-zero levels, although they will come down roughly a percentage point by the end of 2024. The high U.S. debt means the Treasury will have to issue more bonds/notes to finance the debt and Treasury yields correlates to the 30-year mortgage rate (meaning we aren’t likely to see 3% mortgages anytime in the foreseeable future). Lastly, 38% of global GDP economies will have elections in 2024 (more if the U.K. calls an election) and that too introduces more economic and political uncertainty.

But for us, it really is all relative. In the international economic report we do, I talk about the resiliency of the U.S. economy as compared to most other developed nations particularly Europe. Despite the pain that has come with higher interest rates and higher debt levels, the U.S. has fared better than peer nations as Europe will likely be in a recession in 2024. The U.S. GDP growth rate will likely be around 1.0% in 2024 — nothing to write home about — but should resume trend growth of almost 2.0% by 2025. Most households will keep their jobs with unemployment rates around 4.0%, which is quite low by historical standards. And if Colorado Springs can navigate its growing pains, we can outperform most other counties in Colorado and across the nation. Modest reductions in interest rates, improving (University of Michigan) consumer sentiment, and other recent indicators tell me that we may avert recession in 2024 after all, barring any economic shocks. And even with underwhelming growth, that’s good news.

I’ll feel especially optimistic if the Michigan Wolverines beat Alabama on the first day of 2024. Perhaps there are parallels between Michigan football and the U.S. economy? Michigan’s program has the most total wins in college football history (1,002), most appearances in the final AP Poll (62), and most undefeated seasons (23) of any D1 program. There are always headwinds and challenges, but like UM football, the U.S. has outperformed its peers, and that alone is worth celebrating.

Tatiana Bailey

Tatiana Bailey